When dealing with insurance, you may encounter the terms ‘rejected’ and ‘repudiated’ insurance claims. Both involve situations where an insurer decides not to approve a claim, yet the reasons and implications differ significantly. Understanding the difference can help you avoid common mistakes, respond appropriately, and improve your chances of a successful claim. In this article, you will explore what sets rejected claims apart from repudiated ones, common reasons each occurs, and how you can effectively manage or prevent these scenarios.

What is a Rejected Insurance Claim?

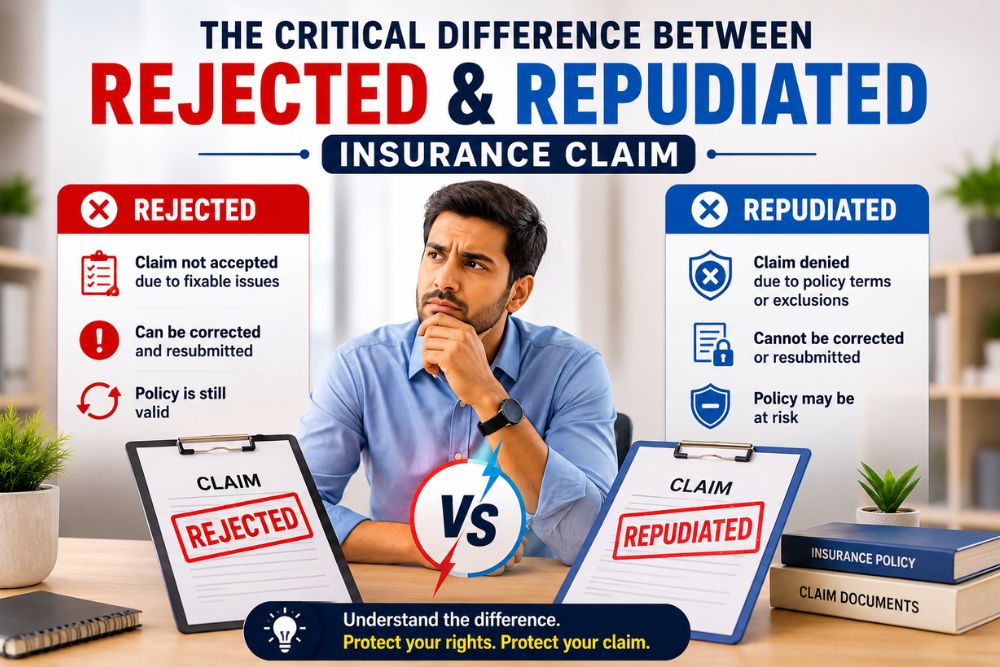

A rejected insurance claim occurs when an insurer does not process a claim because of errors, incomplete information, or missing documents in the claim submission. This rejection typically occurs at an early stage in the claims process and is often a result of procedural issues rather than an outright refusal of coverage.

For example, a health insurance claim may be rejected if it contains an incorrect policy number, missing medical records, or incomplete claim forms. This initial rejection is corrective in nature, aiming to resolve issues so the claim can be resubmitted correctly. It’s important to note that a rejected claim can usually be corrected and resubmitted once the issues identified by the insurer are addressed.

Common Reasons for Insurance Claim Rejection

Understanding why claims are rejected is vital for ensuring compliance and avoiding unnecessary delays. Some of the most common reasons your claim might be rejected include the following:

- Insufficient Documentation: Failing to provide the necessary supporting documents, such as receipts, medical reports, or accident descriptions, can lead to rejection.

- Incorrect Information: Mistakes like wrong policy numbers, misspelled names, or incorrect billing codes can result in a rejection.

- Late Submission: Submitting claims beyond the stipulated time frame set by the insurance company can be grounds for rejection.

- Incomplete Claim Forms: Leaving mandatory sections of the claim form incomplete or providing inconsistent information can result in the claim being rejected.

Carefully reviewing your claim form, submitting all required documents, and meeting the insurer’s timelines can help reduce the risk of claim rejection.

What is a Repudiated Insurance Claim?

A repudiated insurance claim occurs when the insurer reviews the claim and decides it is not payable because it does not meet the policy’s terms and conditions. This decision typically results from findings that the claim does not fall within the coverage provided by the policy, or there are significant disputes about the validity of the claim.

Repudiation is more substantive and often based on an issue of policy coverage or legal terms. For example, if you file a health insurance claim for a treatment that is specifically excluded under your policy or during a waiting period, the insurer may repudiate the claim.

This outcome signifies the insurer’s perspective that even with proper documentation, the claim is not payable for reasons rooted in policy interpretation or agreement violations.

Common Reasons for Insurance Claim Repudiation

Repudiation is typically more serious than rejection and often involves complex disputes. Key reasons for repudiation include:

- Non-Disclosure or Misrepresentation: If it is determined that you provided false or incomplete information when obtaining the policy, the insurer might repudiate a claim.

- Breach of Policy Conditions: Violating terms or conditions of the policy, such as lack of payment of premiums or failure to maintain safety measures, can lead to repudiation.

- Exclusions and Limitations: Claims falling under specific exclusions or exceeding policy limits are often repudiated.

- Fraudulent Claims: Any attempt to claim through false representation or deliberate exaggeration is likely to result in repudiation.

Reading your policy carefully, understanding its exclusions and waiting periods, and providing accurate information can help reduce the risk of claim repudiation.

Key Differences Between Rejected and Repudiated Claims

Understanding the difference between rejected and repudiated insurance claims helps you determine the appropriate steps to resolve the issue. The key differences include:

- Reason for the Decision: A rejected claim is usually caused by documentation or procedural errors, while a repudiated claim occurs because the claim does not meet the policy’s terms, conditions, or coverage.

- Possibility of Resubmission: Rejections allow for resubmission after corrective action, whereas repudiations require an appeal or legal intervention if contested.

- Stage of the Claim Process: Rejections generally occur during the initial review of the claim, while repudiation happens after the insurer completes a detailed assessment.

Understanding these differences can prepare you for the appropriate steps and responses to take when confronted by either scenario.

Steps to Take When Facing a Rejected Claim

Handling a rejected insurance claim efficiently begins with understanding and action. Here’s how you can navigate through it:

- Review the Rejection Notice: Carefully read the insurer’s explanation to identify the reason for the claim rejection and the corrections required.

- Gather Correct Information: Collect the correct documents and information to address the highlighted issues.

- Contact Your Insurer: If the reason for rejection is unclear, contact your insurer or claims representative for clarification and guidance.

- Resubmit Corrected Claim: Once all errors are addressed, resubmit the claim for further processing.

Promptly following these steps helps ensure that your corrected claims are processed without further delays.

Preventing Claim Denials and Repudiations

Prevention is always better than cure, particularly with insurance claims. Here’s a guide to minimizing the risk of claim denials:

- Understand Your Policy: Read your policy carefully, including its coverage, exclusions, waiting periods, and claim conditions, before filing a claim.

- Accurate Filing: Double-check all submissions for completeness and accuracy before filing them.

- Maintain Records: Keep thorough records of all incidents and communications relevant to potential claims.

- Regular Policy Reviews: Conduct timely reviews of your coverage to ensure it still meets your needs and reflects any changes in circumstances.

Following these practices can help reduce the likelihood of an insurance claim being denied, rejected, or repudiated, making the claims process smoother and more efficient.

In conclusion, distinguishing between rejected and repudiated insurance claims is essential for addressing insurance disputes effectively. Rejected claims usually involve easily rectifiable administrative issues, whereas repudiated claims typically require more extensive investigation and often pertain to policy details. By understanding the common causes of both outcomes and following your policy requirements carefully, you can improve your chances of a successful claim and avoid unnecessary delays.

Frequently Asked Questions

1. What is the difference between a rejected and a repudiated insurance claim?

A rejected insurance claim is usually caused by errors such as missing documents, incorrect information, or incomplete claim forms and can often be corrected and resubmitted. A repudiated insurance claim, however, is denied because it does not meet the policy’s terms, conditions, or coverage and may require an appeal if disputed.

2. Can a rejected insurance claim be resubmitted?

Yes. In most cases, a rejected insurance claim can be corrected and resubmitted after addressing the issues identified by the insurer, such as providing missing documents or correcting inaccurate information.

3. Why do insurance companies repudiate claims?

Insurance companies may repudiate claims due to policy exclusions, non-disclosure of important information, violation of policy terms, waiting period restrictions, or fraudulent claims. Repudiation occurs when the claim is not covered under the policy.

4. How can I avoid my insurance claim being rejected or repudiated?

To reduce the risk of claim rejection or repudiation, ensure your claim form is accurate, submit all required documents on time, understand your policy’s coverage and exclusions, disclose all relevant information honestly, and follow the insurer’s claim procedures.

5. What should I do if my insurance claim is repudiated?

If your claim is repudiated, carefully review the insurer’s reason for the decision and your policy terms. If you believe the decision is incorrect, you can submit additional supporting evidence, file a formal grievance with the insurer, or approach the appropriate insurance grievance redressal authority if necessary.